Related Articles

What Is a FICO Score, and How Does It Affect Your Credit?

Jenius Bank Team8/14/2023 • Updated 9/4/2024

Raising your credit score may improve your lending offers. A key part of managing your finances is understanding your credit score and how it impacts your ability to borrow money.Credit scores range from 300 to 850, and the higher the number, the better your credit score is. Two of the leading names in credit scores are VantageScore and FICO. Many lenders rely on the FICO score when determining a borrower’s credit worthiness. Let’s take a closer look at what a FICO score is and how it impacts your ability to borrow money or open new lines of credit.

Key Takeaways

- FICO scores are calculated by the Fair Isaac Corporation and take five main areas into consideration when coming up with a score: payment history, current debts, credit mix, length of credit history, and new credit inquiries.

- Your credit score tells lenders about your creditworthiness and helps them decide if they want to issue you a loan or a new line of credit and the terms associated with that credit.

- Checking your FICO score on a regular basis to monitor your performance could help set you up for financial success in the long run.

What Is a FICO Score?

A FICO score is a type of three-digit number credit score calculated by the Fair Isaac Corporation (FICO), a data analytics company that has been calculating scores for over 30 years.1 Credit scores are used by financial lenders to predict how likely you are to repay debts, particularly loans or credit cards. The higher the score the higher the likelihood. Despite the rise of other credit scoring models, like VantageScore, FICO is still the most common model used by lenders, particularly mortgage lenders.2 FICO has multiple scoring models depending on which credit reporting bureau the information is being pulled from.3 Since the models are slightly different depending on the reporting agency, your FICO score may vary from one lender to another.4FICO vs VantageScore

FICO and VantageScore are the leading credit scoring models in the US. VantageScore was created in 2006 as a joint venture between the three major credit bureaus, TransUnion, Equifax, and Experian.5 Their goal was to create a scoring method that was easier for individuals to understand and use. While FICO remains the most common model among certain lenders, particularly in the mortgage space, VantageScore has become more popular in the past few years, seeing a 46% increase in use among financial and non-financial institutions between 2021 and 2022.6 Some key differences between the two models include how they weigh certain factors, how long a person’s credit history must exist before the model can calculate a score, and how hard inquiries are treated within the model.7What Is a Good FICO Score?

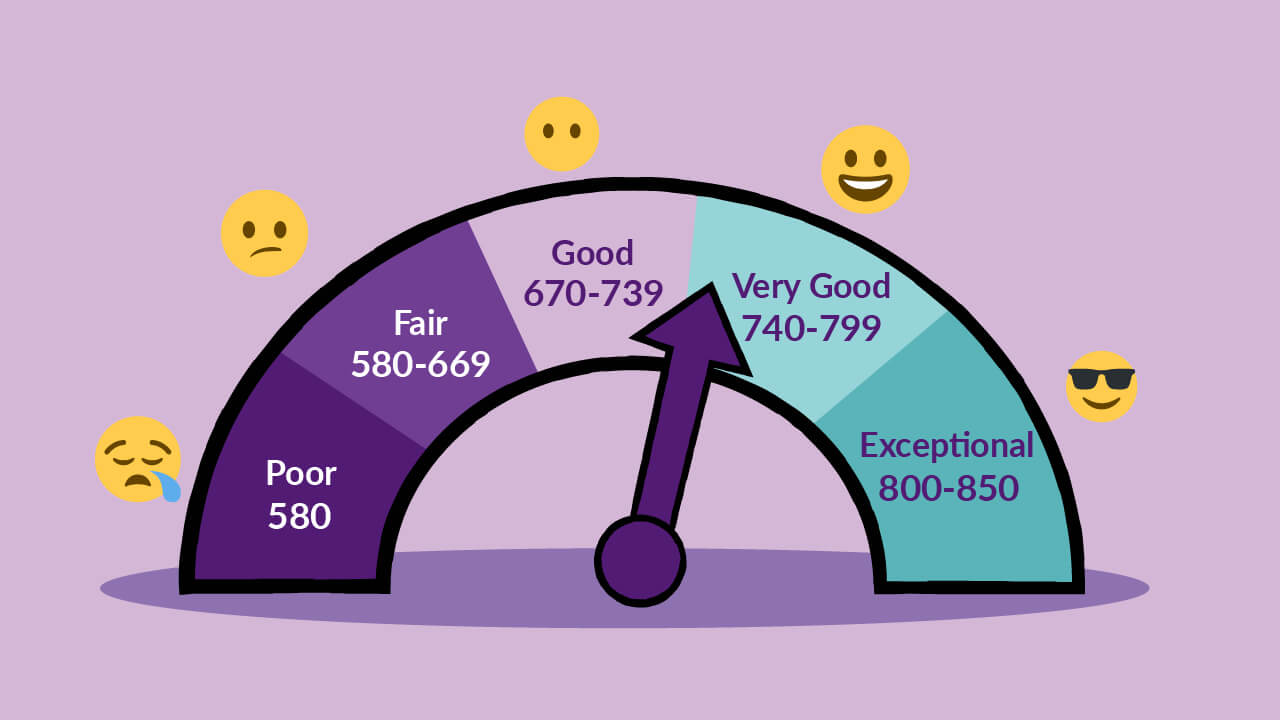

FICO uses a score range of 300 to 850, with a 300 meaning you are a potential credit risk and an 850 meaning you have a strong credit history. Lower scores may make it difficult to qualify for a loan or a new credit card, while high scores may allow you to qualify for higher amounts of credit or receive better terms, such as lower rates. FICO breaks their range into five score bands.8- Poor (300-579): Individuals with Poor scores may struggle to qualify for any type of unsecured financing, such as a personal loan or credit card.

- Fair (580-669): Individuals with Fair scores may be able to qualify for a loan or a new credit card but may have higher rates or lower borrowing limits.

- Good (670-739): Individuals with Good scores are likely able to qualify for new lines of credit or loans with rates close to the market average.

- Very Good (740-799): Individuals with Very Good scores are usually able to easily qualify for a new line of credit or loan with high borrowing limits and lower than market average rates.

- Exceptional (800-850): Individuals with Exceptional scores may experience an easier approval process when applying for new credit, and may be offered market leading lending terms, including low rates and high limits.

How Are FICO Scores Calculated?

FICO scores take several factors into consideration, creating a comprehensive picture of your credit history. These are the components that FICO looks at and how much weight they assign to each component.9- Payment history (35%): The largest factor in your FICO score is your payment history on different accounts, such as credit cards, installment loans and retail accounts. This factor looks at how often you pay bills on time, as well as how often, if ever, you make late payments.

- Amounts owed/outstanding debt (30%): The next largest factor in your FICO score looks at how much money you owe on existing loans and lines of credit. This is often expressed as a credit utilization ratio, which divides how much debt you currently owe by the total amount of credit you have available. The lower your ratio, the less risky you appear to lenders.

- Length of credit history (15%): Your credit history’s length, or how long you’ve had some kind of credit, is another important factor. This history could be student loans, credit cards, or any other type of debt. Note that you need to have an account open for at least six months before FICO can calculate a score.

- Recent inquiries (10%): Anytime you apply for a loan or a new line of credit, the lender does a “hard” credit check to see what your score is. Hard credit checks are recorded on your credit report and stay on it for two years. Higher numbers of inquiries may negatively impact your score, particularly if several inquiries occurred in a short period of time. When you’re pre-approved for a loan offer, a lender performs a “soft” inquiry. These types of inquiries don’t impact your credit score. Bottom line, be sure to ask when someone pulls your credit what type of pull it will be… it may make a difference in your credit score.

- Credit mix (10%): Having a mix of credit types, such as revolving debt like credit cards and installment loans are beneficial for your score.

Why Are FICO Scores Important?

FICO scores are an important benchmark that lenders use when reviewing applications for new loans or lines of credit. If you don’t know what your credit score is, you may be surprised when you apply for a loan. If your score is lower than you thought, you may not be eligible for the amount you’re asking for or the terms offered may not be as great as you’d hoped.If you know what your score is before you apply for credit, and you’re able to review the lender’s requirements, you’re able to decide if you should continue with the application or wait until your score has improved.For example, if your score is low, you may not qualify for a new loan or line of credit, or you may have to pay higher than average rates. But if you take the time to improve your score, you may boost your chances of approval, or be offered better terms in a matter of months.How Could I Improve My FICO Score?

The factors that contribute to your credit score are tied to your overall financial behavior. If you haven’t always made the best financial decisions, your FICO score may be lower than you’d like.So, how could you increase your score? The FICO scoring system rewards good habits. To improve your credit score, here are a few steps you could take.- Make on-time payments for every debt or bill you have.

- Keep your total credit utilization under 30%, meaning don’t use more than 30% of your total available credit. Thirty percent is the ratio most experts recommend,10 but usually the lower the ratio, the better your score.11

- Pay down what you owe until you stop carrying a balance, particularly on credit cards, to help lower your credit utilization ratio.

- Try to avoid applying for multiple new debts at once—either opening credit cards or taking out new loans—to keep your total number of hard inquiries lower.

- Making late payments or missing payments entirely.

- Using too much of your available credit or maxing out your credit cards, resulting in a high credit utilization ratio.

- Carrying a credit card balance each month.

- Opening multiple new lines of credit or applying for new loans often, increasing the number of hard inquiries made on your behalf.

How Do I Check My FICO Score?

Understanding what your FICO score is may be helpful, but it’s not helpful if you don’t know how to check it.Luckily, it’s fairly easy to check your FICO score. Here are some of the easiest methods to try.- Ask your lender: If you’ve applied for a loan or a new credit card and the lender has run a credit check, you’re able to request a copy of that report. The report should tell you exactly what your score is.

- Visit the FICO website: The FICO website allows you to check your FICO score for a fee.

- Use a personal finance site: Many personal finance sites provide free access to your credit score and let you check it as often as you want. And contrary to some myths out there, checking your credit score doesn’t cause your score to drop.

- Check with your bank or credit card provider: You may be able to request a copy of your credit score for free. Keep in mind that not all banks and credit card providers offer this service.

Final Thoughts

Your FICO score is a quick way for lenders to determine your creditworthiness. The higher your score is, the more likely it is that you would qualify for a loan or a new line of credit. By understanding how FICO scores work and what you are able to do to keep your score as high as possible, you may be on your way to long-term success.Banking 101Financial Wellness